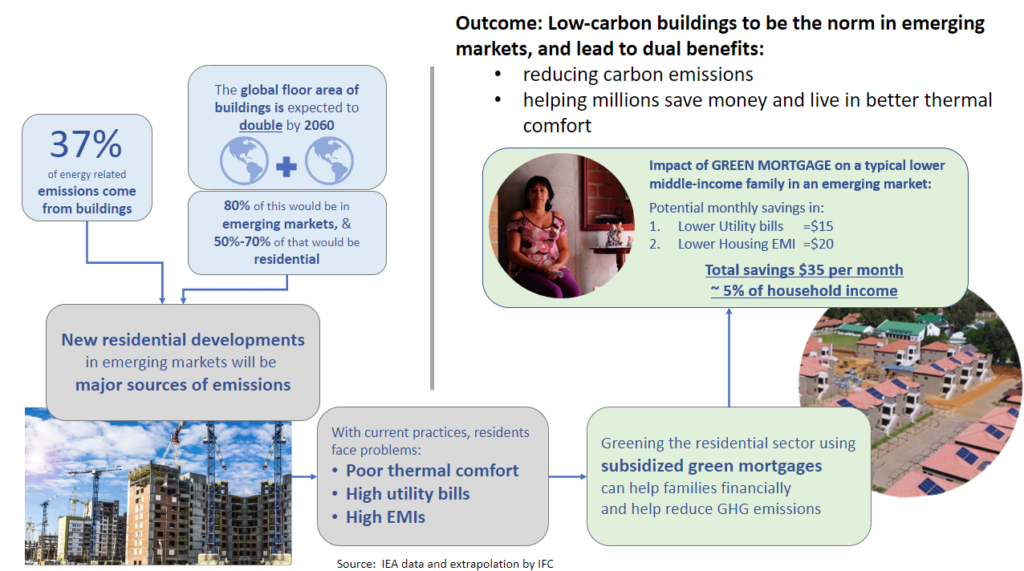

Background: The buildings sector is responsible for 37% of all energy-related GHG emissions. By extrapolating annual growth in the total floor space in the world, it is expected that the total built-up floor area in the world today will double by the year 2060. Approximately 70% of this new construction will be residential, primarily in emerging markets. Unless the residential sub-sector is addressed and transitioned en-masse towards low carbon, a meaningful reduction in total emissions from the buildings’ sector will not be possible.

The good news is that the know-how and the technologies for reducing operational and embodied emissions in new residential buildings not only exist but are easily available. The incremental costs of these green buildings typically range from 1% to 3% when compared with business-as-usual buildings and usually get paid back in 1-3 years through savings in utility costs.

IFC’s EDGE App is one such tool that anyone anywhere in the world could use, free of cost, for assessing the resource efficiency of their existing or new buildings. By design, the EDGE Buildings system is not prescriptive, and users can choose green measures best suited to their specific situation or need to increase resource efficiency and reduce GHG emissions.

Challenges: Lack of awareness and information asymmetry are probably the biggest challenges in mainstreaming green residential construction in emerging markets. Most home buyers are not aware of the cost-benefit advantages and hence are not asking for it. The developers, even if aware, are not inclined to build green as the cost will be borne by them whereas the benefits will go to the home buyers. Most also have the misperception of costs being much higher than they are.

The impact of supply-side interventions such as green construction loans is limited only to the investee projects and hence is not transformative in nature.

Solution: Demand-side interventions such as green mortgages have shown great promise for large-scale transformative impact in the residential sub-sector. Several of IFC’s investments with financial institutions have resulted in green mortgage products launched by those FIs and they have shown promising results in moving the residential market towards green. The transformation in the country of Colombia is a great example, where ~30% of all new construction now gets certified as green, up from less than 1% just seven years ago. Similar progress is now seen in South Africa with ~13% of new construction getting green-certified. Several banks in both countries have started offering green mortgages with preferential rates in the last few years.

Green mortgages that offer an interest rate reduction of 50 to 100 basis points, even if just for the first 5 or 6 years, generate great interest from customers, thus creating a strong demand-side pull for green homes.

When deployed at scale in a concerted manner, such green mortgages can become a powerful lever that creates a demand-pull that is exponentially bigger than the amount of green finance being deployed and therefore, can transform the residential real estate market in a country.

Shifting the Paradigm: Quite often, changes brought about through subsidies are not permanent. However, this is not the case for green buildings. The business case for green buildings is very compelling but information asymmetry, and misalignment of interests, between developers and homebuyers prevents them from being the norm. Green mortgages create a demand pull and in turn, increase awareness among homebuyers. Increased buyer awareness at a market-wide level, makes this change permanent. The lower rates attract the home buyers, and they become aware of the benefits of green homes, such as lower utility bills and better thermal comfort. When green mortgage offerings are widely deployed and dominate the market for a period of 5-6 years, the awareness of these benefits spreads well among homebuyers. They would demand green homes for these benefits, even if there is no reduction in interest rates, thus permanently shifting the market towards green. A well-concerted, large scale market intervention through lower-rate green mortgages could be transformative and transition the whole residential sub-sector to green and low carbon.

Footing the Bill: The question arises, who bears the cost for these interest rate subsidies? Before we delve into that, it must be highlighted that the interest rate reduction does not need to be for the entire tenure of the loan, which typically is 15 to 30 years. The 0.5% to 1% reduction in interest rates could be just for the first 5 or 6 years, a period which the homebuyers care about the most. This significantly reduces the overall cost of interest rate subsidy while retaining its attractiveness for home buyers.

There are two ways to finance the cost of interest rate reduction for green mortgages.

Private Sector Intervention – Blended Finance: A method that is already proven at smaller scales, and could be driven by the private sector, is the use of blended finance that combines regular loans with small portions of non-repayable grants. A good simile would be a drop of blue ink in a glass of water makes the whole glass blue. Similarly, a small amount of a grant creates an incentive for the home buyer to shop for a green home, thus making their mortgage a green mortgage. The grant component is used to subsidize a small portion of the interest for the home buyer, say 0.75% on a 7% home loan for the first six years of the loan.

This translates to a typical subsidy equal to about 5% of the loan value. While this may seem like a huge cost when extrapolated for a whole country’s market, that is not the case. In our estimates, the demand side pull will cause an impact that is ~10 times larger than the actual number of green mortgages deployed, provided it is done at scale in a concerted manner.

Let us elaborate on that. If the top 7-10 home loan companies in a country launch such green mortgage products, it will stir the market as many customers will start asking for these subsidized mortgages. This will cause almost all developers, who compete for these customers, to figure out how they could make their project green. Once they realize that the incremental cost of green measures is just around 1% to 2% of the construction cost, they will choose to build green. Hence, the impact will be disproportionately larger than the actual number of green mortgages deployed in the market, probably by a factor of 10 if not more. This means, that for a $10 billion a year home loan market, only approx. $10 million/year is required in grant money for about five years for it to result in market transformation to green.

The key however is that the intervention needs to be concerted and large scale to make a sizable enough splash in the market.

Policy Level Intervention – Zero-Sum Transformation: Another option for deploying green mortgages as a lever for transformation requires a policy-level intervention. It is arguably more difficult to implement. However, if done right, could be very effective and would not put a financial burden on any specific stakeholder.

In most countries, the residential market is driven primarily by home mortgages and the interest rates for these mortgages depend on many macro and micro factors. The proposed policy intervention would require all financial institutions that originate home loans to achieve a difference in average interest rates for green and ‘non-green’ home loans. The financial institution would be free to choose their pricing but just need to create a differential between the regular and green mortgages. Again, this reduction in rate for green mortgages could be front-loaded on the first few years of the loan tenure. Such policy intervention would not put any financial burden on the banks or the government, just on the non-green projects. Initially, most of the banks’ loans would be non-green, and over 5-7 years the majority would move towards green, always allowing the banks to adjust their pricing so that there is no loss of revenue or market share. Since it will be a policy requirement, all financial institutions are affected therefore the playing field always remains level. Over time all projects being developed will become green.

Conclusion: Interest-subsidized green mortgages, whether delivered through blended finance or policy intervention, provide a great opportunity to transform the residential sector into a low-carbon one. The transition will not only help in addressing climate change but also help millions directly, by reducing their utility bills and enhancing thermal comfort in their homes.

While the policy approach seems to be more effective and comprehensive, it may be harder to implement due to complexities in enforcement and monitoring. Each borrower has a different risk profile and is therefore offered different rates. Implementing a policy that requires different ‘average’ interest rates could be difficult to calculate as other risk factors in both pools would never be the same. Policy measures also face obstacles due to political reasons.

On the other hand, the blended finance approach is entirely controlled by the private sector, potentially led by development banks. The results could be just as transformative without the complexities. A portion of the grants, for example, 5%, could be used for capacity building within the banks to educate property developers, especially in dispelling the myth that green buildings cost significantly more. The blended finance approach could be a more practical way to enable transformative change in the residential sector.

Green mortgages offer a unique opportunity to have a market-wide transition towards low-carbon buildings. However, the effectiveness will depend on whether the intervention is done in a concerted manner to achieve effects at a much larger scale than the intervention itself.